1.1

Rules 3.7.1 and 3.9.1 require Remote Trading Members to have in place adequate tools and procedures to monitor their exposure to a single customer or single security.

Added on 3 June 20193 June 2019.

1.2

A Remote Trading Member may be required to demonstrate the adequacy of such tools and procedures. This Practice Note explains the tools and procedures that a Remote Trading Member may have in place to satisfy the requirement for adequate tools and procedures.

Added on 3 June 20193 June 2019.

2.1

Tools and procedures to monitor a Remote Trading Member's exposure to a single customer or single security that SGX-ST deems adequate include, but are not limited to the following:

Added on 3 June 20193 June 2019.

2.2

SGX-ST shall have the right to require a Remote Trading Member to demonstrate the adequacy of such tools and procedures as it deems necessary.

Added on 3 June 20193 June 2019.

1.1

Rule 3.10.9 requires a Trading Member to review all margin financing accounts carried on its books daily to ensure that credit is not over-extended beyond the approved facility limits and that the margin financing requirements and limits prescribed in Rule 3.10 are met at all times. The Rule also requires the Trading Member to establish and maintain a robust framework to govern the conduct of such reviews.

Added on 1 April 2025.

1.2

This Practice Note sets out SGX-ST’s expectations on the matters that should be included in the framework.

Added on 1 April 2025.

2.1

To ensure that the review of margin financing accounts is robust, the framework include at least the following:

- Policies and procedures to be put in place for determining the suitability and valuation of acceptable collateral;

- Concentration limits to be set at security and single customer level to prevent the firm from taking on excessive risks;

- Performance of timely monitoring of adverse news and market developments to identify potential matters that may impact the valuation of collaterals (e.g. trade with caution alerts, trade suspension, corporate actions); and

- Performance of daily mark to market of margin collateral and daily margin calls to restore margin ratios.

Added on 1 April 2025.

2.2

The Trading Member should review its policies at least annually and during times of market volatility, to ensure the suitability of acceptable collateral and their valuation.

Added on 1 April 2025.

2.3

For the purposes of paragraph 2.1, “single customer” shall have the same meaning ascribed to it in Rule 3.6.6.

Added on 1 April 2025.

2.4

The framework should provide, for the purpose of computing margin financing requirements in a margin financing account, that:

- all transactions done on the same day shall be combined on a transaction date basis;

- the total cost of purchase or the net proceeds of sale, including any commission charged and other expenses, shall be taken into account; and

- the Trading Member may use either:

- the last done price of the Specified Product on the preceding Market Day, or in the case of a Prescribed Instrument, the closing price of the Prescribed Instrument on the preceding Market Day, or

- the market price of the Specified Product at the point of calculation on the current Market Day. Where the Trading Member uses real-time market prices for margin valuation, computation of margin financing requirements and issuance of margin calls where required should be carried out at the same time.

Added on 1 April 2025.

2.5

The framework should require that there be a determination of the suitability and valuation of the margin collateral in a margin financing account and require that the following factors be taken into account for that purpose:

- type and quality of margin collateral;

- price volatility of margin collateral;

- where the margin collateral is listed or traded in a foreign jurisdiction or is cash in a foreign currency, matters such as:

- exchange rate volatility,

- ease of liquidating collateral in the foreign jurisdiction, and

- differences in legal and regulatory framework between such foreign jurisdiction and Singapore; and

- where the margin collateral is custodised in a foreign jurisdiction, matters such as:

- risks arising from differences in custody arrangements in such foreign jurisdiction; and

- treatment of, or legal protection afforded to, customer collateral in the foreign jurisdiction, e.g. prohibition of title transfer for retail customer collateral.

Added on 1 April 2025.

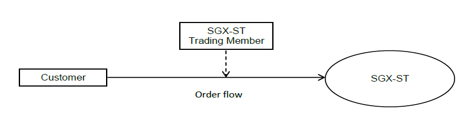

1.1

This Practice Note provides further guidance on the definitions of Direct Market Access and Sponsored Access as used in Rule 4.2.

Added on 3 June 20193 June 2019.

2.1

Direct Market Access may take place in the following manner:

Added on 3 June 20193 June 2019.

1.1

Rule 4.9.3 provides that a Trading Member must have processes in place to minimise and manage conflicts of interest, including but not limited to separating its front and back office functions.

Added on 3 June 20193 June 2019.

1.2

This Practice Note provides guidance on how front office and back office functions of Trading Members should be separated.

Added on 3 June 20193 June 2019.

2.1

The purpose of separating a Trading Member's various key functions is to minimise and manage conflicts of interests among these functions.

Added on 3 June 20193 June 2019.

2.2

Examples of proper separation include:

Added on 3 June 20193 June 2019.

2.3

The basis for determining and amending trading limits should be properly documented. Adequate audit trail reports should be maintained to show all changes to trading limits, the date and time of the modifications and the authorised person who approved the changes. In addition, sufficient checks and procedures should be in place to ensure that all limits and parameters set and modified by the credit control administrator are accurate and have been approved.

Added on 3 June 20193 June 2019.

1.1

Rule 4.10.1(b) requires Trading Members to ensure that adequate pre-execution risk management control checks are conducted, including automated credit control checks on every order and trading limits for each Trading Representative.

Added on 3 June 20193 June 2019.

1.2

This Practice Note sets out the types of pre-execution checks contemplated in Rule 4.10.1(b).

Added on 3 June 20193 June 2019.

2.1

The purpose of requiring Trading Members to ensure that adequate pre-execution risk management control checks are conducted is to prevent overtrading and for credit risk management. As such, the checks must be appropriately set to effectively limit the firm's risk exposure arising from every order (including proprietary orders) to prevent the taking on of excessive risk.

Added on 3 June 20193 June 2019.

2.2

The parameters of such pre-execution checks and filters may include but are not limited to:

Added on 3 June 20193 June 2019.

2.3

By way of illustration, pre-execution risk management control functions may include the following:

Added on 3 June 20193 June 2019.

2.4

Trading Members who authorise Sponsored Access will be able to meet the requirement in Rule 4.10.1(b) by being able to directly set and control pre-determined automated limits in the Sponsored Access customer's system, having automated alerts whenever such limits are altered, and by conducting regular post-execution reviews of trades. Trading Members should assess and continue to ensure that the pre-execution risk management control checks are robust on an ongoing basis.

Added on 3 June 20193 June 2019.

2.5

Where a Trading Member has allowed its Clearing Member to directly set and control pre-determined automated limits in the Trading Member's system, the Trading Member should have the appropriate internal controls to prevent unauthorised modification of the limits set by the Clearing Member.

Added on 3 June 20193 June 2019.

1.1

Rule 4.10.1(c) requires Trading Members to have error prevention alerts to bring attention to possible erroneous entries of price, order size and other data fields.

Added on 3 June 20193 June 2019.

1.2

This Practice Note explains the types of error-prevention alerts contemplated in Rule 4.10.1(c).

Added on 3 June 20193 June 2019.

2.1

The purpose of requiring Trading Members to have error prevention alerts is to give Trading Members the opportunity to review the order and confirm its accuracy before it is transmitted to the Trading System for matching.

Added on 3 June 20193 June 2019.

2.2

The types of error-prevention alerts to be made available may include but are not limited to the following:

Added on 3 June 20193 June 2019.

2.3

Price alerts. Price alerts should trigger when the order price is far away from the prevailing market price in that it deviates by:

as compared to the prevailing market price. The prevailing market price may be the last traded price, the previous settlement price, the closing price or the opening price, as appropriate.

Added on 3 June 20193 June 2019.

2.4

Order size alerts. Order size alerts should trigger when the order size exceeds a pre-set threshold. The threshold may be set in terms of quantity or value of an order.

Added on 3 June 20193 June 2019.

2.5

Other data field alerts. Other data field alerts may include order type alerts that would trigger when an order is of a type that differs from other orders existing in the market (e.g. a buy order instead of a sell order).

Added on 3 June 20193 June 2019.

Practice Note 4.10.2 Firm Level Monitoring of Capital and Financial Requirements and Prudential Limits

1.1

Rule 4.10.2 provides that a Trading Member must have automated processes and procedures in place to monitor at the firm level if the Trading Member is at risk of breaching capital and financial requirements and prudential limits on exposures to a single customer and a single security, so as to restrict trading activity, inject additional capital or take such steps as are necessary to prevent such breach.

Added on 3 June 20193 June 2019.

1.2

This Practice Note explains the requirement for monitoring potential breaches of capital and financial requirements and prudential limits on exposures to a single customer and a single security.

Added on 3 June 20193 June 2019.

2.1

In an electronic trading environment where orders are processed and routed at speed, Trading Members should use appropriate measures to monitor if the firm is at risk of breaching its capital or financial requirements or any prudential limits, for example:

Added on 3 June 20193 June 2019.

1.1

Rule 4.12 requires Members to:

Added on 3 June 20193 June 2019.

1.2

The objective is to ensure that Members have the ability to:

Added on 3 June 20193 June 2019.

2.1.1

Rule 4.12.1 requires Members to maintain adequate business continuity arrangements, and document such arrangements in a business continuity plan. As a guide, a Member's business continuity plan should document the following elements:

Added on 3 June 20193 June 2019.

2.2.1

A Member should establish and maintain a crisis management plan as part of its business continuity plan. The crisis management plan should include (but not be limited to):

Added on 3 June 20193 June 2019.

2.2.2

SGX-ST may declare a wide-area crisis in the event of a major and widespread incident. When such declaration is made, SGX-ST may require a Member to submit status reports to SGX-ST. A wide-area crisis may include any incident where the operations of a large number of market participants are disrupted simultaneously.

Added on 3 June 20193 June 2019.

2.3.1

Rule 4.12.1 also requires a Member to review and test its business continuity plan regularly. Members should do so at least once a year to ensure that their business continuity plans remain relevant.

Added on 3 June 20193 June 2019.

2.3.2

Where there are material changes to a Member's business activities and operations, the Member should update its business continuity plan accordingly. Regular training should be conducted for staff to be updated and aware of any relevant changes to the Member's business continuity arrangements. As a principle, training should be conducted when:

Member firms should also conduct refresher courses for existing staff where appropriate.

Added on 3 June 20193 June 2019.

2.4.1

The features of a business continuity plan set out in paragraphs 2.1, 2.2 and 2.3 may not be applicable to a Remote Trading Member. A Remote Trading Member should meet any applicable business continuity plan requirements that are prescribed by its Relevant Regulatory Authority. The Trading Member may further adopt the recommended features of a business continuity plan set out in this Practice Note 4.12.

Added on 3 June 20193 June 2019.

3.1

Rule 4.12.3 requires a Trading Member to appoint emergency contact persons and furnish the contact information of such persons to SGX-ST. Members may appoint an emergency contact person and up to two alternates. A template is attached as Appendix A to this Practice Note for the notification of contact information (postal address, email, telephone, mobile telephone and facsimile numbers) to SGX-ST.

Refer to Appendix A of Practice Note 4.12.

Added on 3 June 20193 June 2019.

3.2

Members are to ensure that the contact information provided to SGX-ST is updated on a semi-annual basis. Nonetheless, where there are changes to a Member's emergency contact persons and contact information, the Member should notify SGX-ST immediately in writing.

Added on 3 June 20193 June 2019.

3.3

A Member's authorised emergency contact person should immediately notify SGX-ST in the event where:

Added on 3 June 20193 June 2019.

Appendix A to Practice Note 4.12 Business Continuity Management Emergency Contact Person(s)

Business Continuity Management Emergency Contact Person(s)

Company Name: ____________________________

| Name | Department | Designation | Office No. | Mobile No. | E-mail Address |

Prepared by:

_____________________________

Name:____________________________

Designation:_______________________

Added on 3 June 20193 June 2019.

Practice Note 4.15.2(a) and (b) Opening of Customer Accounts: Obtaining Adequate Particulars, Verification of Identity, and Verification of Authority to Trade

1.1

Rules 4.15.2(a) and (b) state that prior to opening a customer account, a Trading Member shall satisfy itself that it has (a) obtained adequate particulars of each customer, and (b) verified the identity of each customer, and in the case of a non-individual customer verified that it is validly constituted and that the person opening the account has the requisite authority to do so, and in the case of an agency customer, verified the identity of the principal and the customer's authority to trade for its principal.

Added on 3 June 20193 June 2019.

1.2

This Practice Note sets out some of the ways in which a Trading Member may comply with its obligations under Rule 4.15.2(a) and (b).

Added on 3 June 20193 June 2019.

2.1

The particulars that a Trading Member may obtain include the following:

Added on 3 June 20193 June 2019.

2.2

If the customer does not open the account in person, a Trading Member should take suitable steps to verify the customer's identity. The Trading Member may employ one or more of the following means to establish the customer's identity:

Added on 3 June 20193 June 2019.

3.1

The particulars that a Trading Member may obtain include the following:

Added on 3 June 20193 June 2019.

4.1

A Trading Member is encouraged to explore the use of digital signatures for online identification and verification. The identification and verification procedures for acceptance of digital signatures must be at least as rigorous as those which a Trading Member would normally have employed.

Added on 3 June 20193 June 2019.

1.1

Rule 4.15.2(d) states that prior to opening a customer account, a Trading Member shall satisfy itself that it has understood each customer's risk appetite and investment objectives (if applicable).

Added on 3 June 20193 June 2019.

1.2

This Practice Note provides guidance on the procedures to understand a customer's risk appetite and investment objectives.

Added on 3 June 20193 June 2019.

2.1

Investment objectives of a customer would include:

Added on 3 June 20193 June 2019.

2.2

Trading Members that hold a Capital Markets Services Licence should bear in mind the effect of Sections 274, 275 and 276 of the SFA. If a customer wants to trade in a security that is offered in reliance on the exemptions under Sections 274 or 275 of the SFA, Trading Members should:

Added on 3 June 20193 June 2019.

2.3

For the avoidance of doubt, the above requirements are applicable to the trading of global depository receipts ("GDRs") which are offered in reliance on the exemptions under Sections 274 or 275 of the SFA. Trading Members should also observe relevant provisions of the Listing Manual in relation to GDRs.

Added on 3 June 20193 June 2019.

2.4

All the documents obtained under paragraph 2.2(b) should form part of the permanent records of the Trading Members. If the customer's account carried on the books of the Trading Member is closed, the documents should be kept for at least the minimum period required by law.

Added on 3 June 20193 June 2019.

1.1

Rule 4.15.2(a) provides that prior to opening a customer account, a Trading Member shall satisfy itself that it has obtained adequate particulars of each customer. Such particulars include the age of the customer.

Added on 3 June 20193 June 2019.

1.2

Rule 4.15.3 provides that before opening a customer account for a customer under the age of 21 ("Young Investor"), a Trading Member shall assess the customer's suitability to trade and disclose the risks of trading to the customer.

Added on 3 June 20193 June 2019.

1.3

This Practice Note provides guidance on how a Trading Member shall assess a Young Investor's suitability to trade and disclose the risks of trading to the Young Investor and also sets out the measures and operational procedures that Trading Members should take as part of good business practice when Young Investors open securities trading accounts with them.

Added on 3 June 20193 June 2019.

2.1

When a Young Investor opens an account carried on the books of the Trading Member, the Trading Member should undertake the following procedures, in addition to their own account opening procedures, and give appropriate emphasis to the following:

Added on 3 June 20193 June 2019.

3.1

Trading Members should ensure that the relevant staff members are adequately trained and familiar with the safeguards put in place for Young Investors. Similarly, any additional procedures should be communicated to all Trading Representatives to ensure proper adherence and consistent application.

Added on 3 June 20193 June 2019.

3.2

In addition, a senior executive should be appointed to oversee and take responsibility for managing all issues relating to Young Investors. This includes monitoring the Trading Member's dealings with the Young Investors and making appropriate adjustments to the procedures and processes, where necessary.

Added on 3 June 20193 June 2019.

4.1

Trading Members should offer basic investment courses to Young Investors, as well as product-specific courses to those who wish to trade in more sophisticated instruments and products. These courses will enable Young Investors to be more aware of the implications of their trading decisions and to be able to make better investment choices.

Added on 3 June 20193 June 2019.

4.2

Such courses may be organised or conducted by third party course providers or in-house trainers.

Added on 3 June 20193 June 2019.

1.1

Rule 4.15.5 provides that at least one member of senior management or delegate staff (whether of the Trading Member or the Trading Member’s related corporation or otherwise) independent of the Trading Member’s sales or dealing, must approve the opening of a customer account carried on the books of the Trading Member.

Added on 24 March 202024 March 2020.

1.2

This Practice Note provides guidance on how a Trading Member may satisfy the above requirement.

Added on 24 March 202024 March 2020.

2.1

A Trading Member will be deemed to have obtained the approval of senior management or delegate staff independent of the Trading Member’s sales or dealing for the opening of a customer account if:

Added on 24 March 202024 March 2020.

2.2

In the spirit of the rule, the pre-defined approval criteria should minimally address the risks posed by the client with regard to credit, money laundering and terrorist financing.

Added on 24 March 202024 March 2020.

2.3

An example of a set of pre-defined approval criteria is as follows:

Added on 24 March 202024 March 2020.

2.4

It is strongly recommended that the Trading Member should have in place:

Added on 24 March 202024 March 2020.

1.1

Rule 4.18 states that save for Accredited Investors, Institutional Investors and Expert Investors, a Trading Member must provide its Internet Trading customers with adequate information, guidance and training on (a) prohibited trading practices; (b) potential limitations and risks of Internet Trading; (c) system functionalities and order management procedures; and (d) market conventions such as minimum bid sizes and board lot sizes. With respect to Accredited Investors, Institutional Investors and Expert Investors, a Trading Member's obligation relates solely to the provision of adequate information in relation to prohibited trading practices.

Added on 3 June 20193 June 2019.

1.2

This Practice Note provides guidance on the information that a Trading Member should provide to its Internet Trading customers.

Added on 3 June 20193 June 2019.

2.1

A Trading Member should provide its Internet Trading customers with adequate information, guidance and training with respect to the areas below.

Added on 3 June 20193 June 2019.

2.2

Prohibited trading practices, which refer to trading practices prohibited under these Rules, the SFA or other Singapore laws.

Added on 3 June 20193 June 2019.

2.3

Potential limitations and risks of Internet Trading, which include:

Added on 3 June 20193 June 2019.

2.4

System functionalities and order management procedures, which include:

Added on 3 June 20193 June 2019.

2.5

Market conventions, which include:

Added on 3 June 20193 June 2019.

1.1.

Rule 4.24.3(c) requires that a Trading Member, before issuing contract notes in electronic form, must obtain the customer's prior revocable and informed consent for receipt of contract notes in electronic form. The Trading Member must retain evidence of the customer's consent. To constitute informed consent, a customer must be told of the manner of delivery and retrieval of the electronic record and any costs that may be incurred.

Added on 3 June 20193 June 2019.

1.2.

This Practice Note provides guidance on how a Trading Member may show evidence of informed consent.

Added on 3 June 20193 June 2019.

2.1.

To show evidence of a customer's informed consent for receipt of contract notes in electronic form, a Trading Member may maintain records to show that the customer had been given adequate prior notice of the cessation or non-provision of paper statements and had been provided with instructions on how to opt out of electronic-only statements.

Added on 3 June 20193 June 2019.

1.1

Rule 4.38.1 says that a Trading Member and its Trading Representatives may receive goods and services from a broker for directing business to the broker under certain conditions.

Added on 3 June 20193 June 2019.

1.2

Rule 4.38.2 says that a Trading Member may pay for goods and services to a customer for directing business to the Trading Member under certain conditions.

Added on 3 June 20193 June 2019.

1.3

This Practice Note provides guidance on the types of goods and services that do not qualify for soft dollar receipts or payments.

Added on 3 June 20193 June 2019.

2.1

The following goods and services do not qualify as acceptable soft dollar receipts or payments for the purpose of Rule 4.38:

Added on 3 June 20193 June 2019.

2.2

A Trading Member or its Trading Representative should not receive goods and services from a broker, if the act of it compromises the interest of the customer or may result in the breach of the Rules or other regulatory requirements by the Trading Member or its Trading Representatives.

Added on 3 June 20193 June 2019.

1.1

Rule 5.7.1 states that save in specified situations, neither a Trading Member nor a Trading Representative shall deal in securities or futures contracts for its own account or for a Prescribed Person's account if the Trading Representative has an unexecuted order on the same terms from a customer.

Added on 3 June 20193 June 2019.

1.2

Rule 5.7.2 defines "Prescribed Person" as including a person, a group of persons, a Corporation or a group of Corporations, or family trusts, whom the Trading Member, or any Director, Officer, Trading Representative, employee or agent of the Trading Member is associated with or connected to.

Added on 3 June 20193 June 2019.

2.1

An order includes an order for a single stock futures contract or futures contracts.

Added on 3 June 20193 June 2019.

2.2

An unexecuted order from a customer includes an order that has been received but not entered into the Trading System.

Added on 3 June 20193 June 2019.

2.3

"On the same terms" includes:

Added on 3 June 20193 June 2019.

2.4

The Trading Member or Trading Representative must ensure that customers' orders are not compromised when squaring off a house error position on the same terms. Where the customer's order is a careful discretion order, trades allocated to the customer's account must not be worse off to that allocated to the house error account (such accounts being accounts carried on the books of the Trading Member).

Added on 3 June 20193 June 2019.

2.5

In considering whether Rule 5.7.1 has been complied with, the following factors are relevant:

Added on 3 June 20193 June 2019.

3.1

"Prescribed Person" includes a person, group of persons, a Corporation or a group of Corporations or family trusts, whom the Trading Member, Director, employee or Trading Representative of the Trading Member is associated with or connected to.

Added on 3 June 20193 June 2019.

3.2

However, where the Trading Member, Director, employee or Trading Representative of the Trading Member has no control or influence over the associated or connected person, group of persons, Corporation or group of Corporations, or family trusts, they would not fall within the definition of "Prescribed Person".

Added on 3 June 20193 June 2019.

1.1

Confidence in the financial system and effective intermediation of financial flow requires that markets be fair, orderly and transparent. Improper conduct which gives rise to a false or misleading appearance of trading activity, price movements or market information undermines market integrity and erodes investor confidence. SGX-ST seeks to ensure that its markets are fair and orderly and free of manipulative trading.

Added on 3 June 20193 June 2019.

1.2

Trading Members and Trading Representatives must ensure that their trading is conducted in accordance with the SGX-ST Rules and the Securities and Futures Act.

Added on 3 June 20193 June 2019.

2.1

Rule 5.12.1 states that a Trading Member or a Trading Representative must not engage in any course of conduct that is likely to create a false or misleading appearance:

Added on 3 June 20193 June 2019.

2.2

Rule 5.12.1 prohibits false trading and market rigging. This trading misconduct involves an intentional interference with the free forces of supply and demand, such that a distortive effect is created vis-à-vis the market for, or the price of, the security or futures contract traded. This distortive effect occurs as a result of any trading strategy or practice that may be employed in order to artificially manage the market for, or the price of, the security or futures contract concerned.

Added on 3 June 20193 June 2019.

2.3

SGX-ST's determination of whether a course of conduct is likely to create a false or misleading appearance will be made on an objective basis. In other words, the Rule does not require the Trading Member or Trading Representative to have intended to create the false or misleading appearance, or knew that it or he was in fact creating a false or misleading appearance. Rule 5.12.2 identifies the factors that SGX-ST may take into account when making the said determination.

Added on 3 June 20193 June 2019.

2.4

The Rule does not prevent Trading Members and Trading Representatives from carrying out legitimate trading strategies that reflect the forces of genuine supply and demand. However, Trading Members and Trading Representatives must do so bearing in mind their obligations to maintain an orderly market, and to conduct their trading activities with an appropriate degree of care.

Added on 3 June 20193 June 2019.

2.5

Trading Representatives (as licensed professionals) must not act as mere order takers and accept their customers' instructions blindly, without conducting any due diligence.

Added on 3 June 20193 June 2019.

2.6

SGX-ST is unlikely to have concerns if the order or transaction is executed in a proper manner and that there is a legitimate commercial rationale for engaging in the said course of conduct.

Added on 3 June 20193 June 2019.

3. Guidance on Rule 5.12.2

Rule 5.12.2 identifies the factors that SGX-ST may take into account when making the determination of whether a course of conduct is likely to create a false or misleading appearance.

Added on 3 June 20193 June 2019.

3.1

Rule 5.12.2(a): Whether the execution of the transaction is inconsistent with the recent trading activity in the security or futures contract, taking into account prevailing market conditions.

Added on 3 June 20193 June 2019.

3.1.1

Trading Members and Trading Representatives would generally be familiar with the patterns of trading in each security or futures contract. They are therefore expected to exercise judgment, based on their experience and knowledge of trading in the security or futures contract, in assessing the likely impact of a proposed transaction on the market for a security or futures contract. This is especially so if the execution of the transaction would result in a significant change in the price (which is inconsistent with the recent trading activity in the security or futures contract, including the intra-day, daily, weekly or monthly price range) and represent a significant proportion of the daily traded volume in the security or futures contract.

Added on 3 June 20193 June 2019.

3.1.2

The Rule does not prevent a Trading Member or Trading Representative from executing an order simply because it will have an impact on the market for, or the price of, a security or futures contract.

Added on 3 June 20193 June 2019.

3.2

Rule 5.12.2(b): Whether the execution of the transaction is likely to cause or contribute to a material change in the price of, or the market for, the security or futures contract, and whether the person involved or another person with whom the first person is collaborating may directly or indirectly benefit from alterations in the market or price.

Added on 3 June 20193 June 2019.

3.2.1

In the absence of a good reason to buy or sell quickly, customers generally want to obtain the best price. A Trading Member or Trading Representative who receives an order that would materially alter the market for, or the price for, the security or futures contract, should consider whether it is genuine or manipulative.

Added on 3 June 20193 June 2019.

3.2.2

Trading Members and Trading Representatives must also know their customers. Orders placed by a customer or a related party of that customer, who may have an interest in creating a material change in the market for, or the price of, a particular security or futures contract, should be closely examined.

Added on 3 June 20193 June 2019.

3.2.3

Examples:

Added on 3 June 20193 June 2019.

3.3

Rule 5.12.2(c): Whether the execution of the transaction involves the placing of multiple buy and sell orders at various prices higher or lower than the market price, or the placing of buy and sell orders that give the appearance of increased volume.

Added on 3 June 20193 June 2019.

3.3.1

A Trading Member or Trading Representative should not make large entries above or below the prevailing spread to facilitate filling an order on the other side of the market. The placing of buy (or sell) orders at various price steps below (or above) the market may create a false or misleading appearance that the entries are on behalf of genuine buyers (or sellers). The layering of orders also translates into a change in the depth screen and may mislead market participants with respect to interest in the counter.

Added on 3 June 20193 June 2019.

3.4

Rule 5.12.2(d): Whether the execution of the transaction is likely to coincide with or is likely to influence the calculation of reference prices, settlement prices and valuations.

Added on 3 June 20193 June 2019.

3.4.1

A Trading Member or Trading Representative should consider carefully any orders placed with instructions to execute them in or near the Closing Routine, particularly if a price target is set. A Trading Member or Trading Representative should also be alert to orders placed in or near the Closing Routine on the last trading day of the month, quarter or year, or on the expiry dates of options, warrants or futures contracts, which will move the price when executed.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

3.4.2

A customer who, to the knowledge of the Trading Member or Trading Representative, declines the opportunity to obtain a better price during the day and prefers to pay a higher (or lower) price in or near the Closing Routine should be queried as to the strategy. This is important if the order is to buy (or sell) a small volume of the security or futures contract, which is likely to move the price and possibly fix the closing price. Further, if the Trading Member or Trading Representative received a series of similar orders over a number of days, each of which generated a price movement in or near the Closing Routine, the Trading Member or Trading Representative should be satisfied that the customer is not attempting to create a false or misleading appearance with respect to the price of the security or futures contract.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

3.4.3

Examples:

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

3.5

Rule 5.12.2(e): Whether parties involved in the transaction are connected or associated with each other.

Added on 3 June 20193 June 2019.

3.5.1

A concern here might arise if the security or futures contract is held in the name of a colluding party but the market risk actually remains with the seller. There may effectively be no change in beneficial interest.

Added on 3 June 20193 June 2019.

3.6

Rule 5.12.2(f): Whether the order or orders for the purchase (or sale) of a security or futures contract is or are entered with the knowledge that an order or orders of substantially the same size, at substantially the same time, and at substantially the same price, for the sale (or purchase) of the security or futures contract has been or will be entered by or for the same or different parties (excluding Direct Business).

Added on 3 June 20193 June 2019.

3.6.1

The time proximity of orders and the fact that they are for substantially the same price (particularly if the price is out-of-range) and quantity may suggest that the transaction is pre-arranged. Pre-arranged transactions have the effect of creating a false or misleading appearance of active trading, or improperly excluding other market participants from the transaction since the first bid or offer was not adequately exposed to the market.

Added on 3 June 20193 June 2019.

3.6.2

Pre-arranged trading can create an unfair market as it is, in substance, executing risk-free transactions at pre-determined prices rather than at market prices. As the transfer of beneficial interest or market risk (if any) is only between persons who are acting in concert or collusion, there is essentially no legitimate commercial rationale behind pre-arranged transactions. Likewise, a Trading Representative who consistently matches his own buy and sell orders may be considered to have engaged in pre-arranged trading as the transactions are unlikely to be executed for a legitimate economic purpose.

Added on 3 June 20193 June 2019.

3.6.3

The execution of crossings or transactions between the same parties for the same volumes, which are subsequently reversed at the same prices, also raises questions whether the transactions involve a change in beneficial ownership, or are for rollover of trades to extend settlement, or for a purpose of engaging in a circular trading scheme to create the impression of turnover.

Added on 3 June 20193 June 2019.

3.7

Rule 5.12.2(g): Whether the execution of the transaction is likely to cause the price of the security or futures contract to increase or decrease, but following which the price is likely to immediately return to about its previous level.

Added on 3 June 20193 June 2019.

3.7.1

The key question in this area is whether there appears to be any logical trading pattern to the price and volume of the security or futures contract, or whether it seems erratic. Trading is manipulative if it is intended to move the price of the security or futures contract.

Added on 3 June 20193 June 2019.

3.8

Rule 5.12.2(h): Whether the bid (or offer) is higher (or lower) than the previous bid (or offer) but is withdrawn or amended to avoid execution.

Added on 3 June 20193 June 2019.

3.8.1

This could indicate that the order is not genuine, especially where a distinctive pattern of such orders is observed. At the time the bid (or offer) was made, the Trading Member or Trading Representative did not intend to buy (or sell), but intended that the bid (or offer) would not trade and would be withdrawn eventually. Sometimes, such orders are entered to induce buyers (or sellers) into the market to facilitate the filling of an order on the other side of the market.

Added on 3 June 20193 June 2019.

3.8.2

Circumstances that should be carefully reviewed by Trading Members and Trading Representatives include where there is a particularly high ratio of order to trade volume or a record of actively entering and amending orders on both sides of the order book but only trading on one side.

Added on 3 June 20193 June 2019.

3.9

Rule 5.12.2(i): Whether the volume or size of the order or transaction is excessive relative to reasonable expectations of the depth and liquidity of the market at the time.

Added on 3 June 20193 June 2019.

3.9.1

This Rule does not restrict Trading Members and Trading Representatives trading significant volumes where there is a legitimate purpose for the transaction and where the transaction is executed in a proper manner. However, trading significant volumes with the purpose of controlling the price of a security or futures contract will amount to manipulative trading.

Added on 3 June 20193 June 2019.

3.9.2

Example:

A Trading Representative purchased substantial volume in a thinly traded counter, which accounted for a large proportion of the market volume, to establish a predetermined price. Sometimes, this may be followed by up-ticking the bid despite the absence of bona fide investor demand for the security or futures contract.

Added on 3 June 20193 June 2019.

3.9.3

In the same vein, entering excessively large order(s) that is disproportionate to the depth of the order book may be manipulative, as it can create an imbalance between the quantum of demand and supply on the order book and in turn, mislead market participants with respect to interest in the security or futures contract.

Added on 3 June 20193 June 2019.

3.10

Rule 5.12.2(j): Whether the buy (or sell) order is likely to trade with the entire best offer (or bid) volume and part of the offer (or bid) at the next price level.

Added on 3 June 20193 June 2019.

3.10.1

If a customer regularly buys (or sells) on the up-tick (or down-tick) in the face of consistent selling (or buying) pressure, the Trading Member or Trading Representative should query whether the customer is a bona fide purchaser (or seller). Repetitive orders to clear the best offer (or bid) volume, particularly within a short time, suggest that the Trading Member or Trading Representative might be attempting to break the market. The trading spikes or troughs were meant to excite the market and attract spectators to join in.

Added on 3 June 20193 June 2019.

3.11

Rule 5.12.2(k): Whether the buy (or sell) order forms part of a series of orders that successively and consistently increase (or decrease) the price of the security or futures contract.

Added on 3 June 20193 June 2019.

3.11.1

If a customer places a sell order well above the best ask and one or more buy orders which would increase the price towards the customer's ask price, a Trading Member or Trading Representative should query the customer as to the strategy. It may be that the buy orders are intended to get the price running and facilitate the sale at the higher price. Illiquid securities or futures contracts, in particular, are susceptible to this type of improper trading.

Added on 3 June 20193 June 2019.

3.12

Rule 5.12.2(l): Whether there appears to be a legitimate commercial reason for the transaction.

Added on 3 June 20193 June 2019.

3.12.1

Many orders for legitimate commercial reasons can change the market for, or the price of, a security or futures contract when executed. Such orders are acceptable despite the volume and/or price impact, but the Trading Member or Trading Representative must consider any additional intentions that may exist and execute the order in an appropriate manner, bearing in mind its or his obligations, including the requirement to maintain an orderly market.

Added on 3 June 20193 June 2019.

3.12.2

Examples:

Added on 3 June 20193 June 2019.

4.1

SGX-ST expects that Trading Members and Trading Representatives act as "gatekeepers" against market manipulation of any kind. Trading Members and Trading Representatives should provide frontline protection against manipulative activity and not contribute or act as an accessory to such trading misconduct.

Added on 3 June 20193 June 2019.

4.2

In determining whether a course of conduct is likely to create a false or misleading appearance, SGX-ST will make the necessary inference from circumstantial evidence, such as an unusual pattern of trading, as well as a person's interest (whether genuine or ulterior motive) in the security or futures contract in question.

Added on 3 June 20193 June 2019.

4.3

SGX-ST acknowledges that Trading Members and Trading Representatives may not always know if a customer's particular interest in a security or futures contract is genuine or not. However, a Trading Member or Trading Representative who receives an unusual order must be able to establish that it or he has made due enquiries and is satisfied as to the reason for the trading, i.e. taking into account the circumstances of the order, the purpose is unlikely to create a false or misleading appearance.

Added on 3 June 20193 June 2019.

4.4

In the event that a Trading Member or Trading Representative reasonably suspects that an order may be for some other ulterior purpose but continue to facilitate the transaction, the Trading Member or Trading Representative must be aware that its or his contributing act towards the transaction may be unlawful.

Added on 3 June 20193 June 2019.

1.1

Rule 5.12.3 states that a Trading Member or a Trading Representative must not effect, take part in, be concerned in, or carry out, directly or indirectly, any transaction to purchase or sell a security or futures contract, being a transaction that does not involve any change in the beneficial ownership of the security or futures contract as defined in Section 197(5) of the Securities and Futures Act.

Added on 3 June 20193 June 2019.

1.2

Rule 5.12.3 further states that it is a defence if the Trading Member or Trading Representative can show that the purpose or purposes for which it or he purchased or sold the security or futures contract was not, or did not include, the purposes of creating a false or misleading appearance with respect to the market for, or the price of, the security or futures contract.

Added on 3 June 20193 June 2019.

2.1

A transaction that does not involve any change in beneficial ownership will not be considered to be for the purpose or purposes of creating a false or misleading appearance with respect to the market for, or the price of, the relevant security or futures contract if the transaction arises under any of the following circumstances:

Added on 3 June 20193 June 2019.

1.1

Rule 5.12.9 states that a Trading Member must have in place processes to review orders and trades for the purpose of detecting suspicious trading behaviour.

Added on 3 June 20193 June 2019.

1.2

This Practice Note provides guidance on what Trading Members could do as part of their processes for post-execution review of orders and trades.

Added on 3 June 20193 June 2019.

2.1

Trading Members should adopt processes to place suspicious orders and trades on exception reports or to trigger automated alerts for review. Exception reports and alerts should be reviewed by an independent party like a compliance officer or other appropriately qualified person on a regular basis to detect orders and trades or patterns of orders and trades that give rise to the possibility of non-compliance with the Rules and regulations. The review process may involve further enquiry with Trading Representative and/or customers or reviewing other Trading Representative or customer-related information such as past trading activity.

Added on 3 June 20193 June 2019.

2.2

Trading Members are expected to follow up on suspicious orders and trades and keep on file the result of their review process. Where it has been established that has been non-compliance with the Rules and Regulations, or if there is any doubt as to its compliance, apart from reporting such activity to SGX-ST pursuant to Rule 5.12.8, Trading Members are expected to take appropriate action, such as advising the Trading Representative or customer to refrain from such activity, performing a closer monitoring of the Trading Representative or customer and ultimately to close the account carried on the books of the Trading Member if the suspicious activity persists. Trading Members should note that the mere fact that an order has been placed on an exception report does not absolve them from their underlying compliance responsibilities.

Added on 3 June 20193 June 2019.

3.1

The effectiveness of processes to identify suspicious trading behaviour depends to a large extent on the types and size of the parameters set. A list of suggested parameters is below:

Added on 3 June 20193 June 2019.

3.2

Trading Members' processes should be able to identify the above irregular orders/trades regardless of whether they originate from one Trading Representative or customer or a group of Trading Representatives and/or customers acting in concert. In addition, they should also be able to identify consistent patterns of irregular trades done over a period of time.

Added on 3 June 20193 June 2019.

3.3

In setting the above parameters, Trading Members should take note of securities that are illiquid or those with small free floats which make them susceptible to cornering and price manipulation.

Added on 3 June 20193 June 2019.

3.4

Trading Members should also pay attention to orders entered after a corporate action to ensure that the orders reflect the change in price and/or quantity after the corporate action. This is to prevent securities being traded at dramatically wrong prices/quantities due to a lack of knowledge or a misunderstanding of the corporate action by uninformed customers.

Added on 3 June 20193 June 2019.

1.1

Rule 8.11.1 states that SGX-ST may declare publicly a security or futures contract to be a "Designated Instrument" if, in its opinion, there has been manipulation of the security or futures contract (or its underlying), excessive speculation in the security or futures contract (or its underlying), or it is otherwise desirable in the interests of organised markets established or operated by SGX-ST.

Added on 3 June 20193 June 2019.

1.2

This Practice Note explains the circumstances under which SGX-ST may declare a listed or quoted security or futures contract to be a "Designated Instrument".

Added on 3 June 20193 June 2019.

2.1.

SGX-ST has three key regulatory tools to support a fair, orderly and transparent market. They are as follows:

Added on 3 June 20193 June 2019.

2.2

Designation is a tool that is used sparingly and only in exceptional circumstances that warrant such intervention. Such circumstances may include prolonged trading anomalies observed in the security or futures contract, such as order book imbalances and/or prolonged, excessive speculation in a security. The objective of designation is to restore market equilibrium by removing the impact of such anomalies on price formation, and allow the price of the security or futures contract to be formed through demand and supply forces in an informed market. Designation would be lifted once, in SGX's opinion trading has returned to normalcy.

Added on 3 June 20193 June 2019.

3.1

The conditions imposed on a Designated Instrument would depend on the circumstances leading to the designation of the security or futures contract. Examples of such conditions are listed below. One or more of these conditions may be imposed in a particular designation situation, and this list is not exhaustive.

Added on 3 June 20193 June 2019.

1.1

Rule 8.13.1 states that SGX-ST may suspend or restrict trading in any or all listed or quoted securities or futures contracts. It may do so for one or more markets, one or more trading sessions or any part of a trading session in specified circumstances.

Added on 3 June 20193 June 2019.

1.2

Rule 8.15.1 states that a trading halt may be imposed by SGX-ST at the request of an issuer. Rule 8.15.2 states that a trading halt may be imposed by SGX-ST on a security or futures contract when its underlying, or such instrument on the same underlying as SGX-ST may prescribe, is subject to a Cooling-Off Period pursuant to Rule 8.14.2.

Added on 3 June 20193 June 2019.

1.3

This Practice Note explains the characteristics of a suspension and a trading halt.

Added on 3 June 20193 June 2019.

2. Characteristics of a suspension and a trading halt

| Characteristic | Suspension | Trading Halt |

| Initiating party | A suspension can be imposed by SGX-ST under the circumstances stated in Rule 8.13.1. An Issuer may also request a suspension if its request for extension of a trading halt is not approved by SGX-ST. | A trading halt can be imposed by SGX-ST under the circumstances stated in Rules 8.15.1 and 8.15.2. |

| Status of unmatched orders | During a market suspension, unmatched orders in the Trading System may lapse, as determined by SGX-ST. SGX-ST will notify Trading Members of the status of their unmatched orders before the lifting of a market suspension. During a suspension of a single security or futures contract, all unmatched orders will lapse. | During a trading halt, all existing orders in the Trading System remain valid. Orders can still be entered, modified or withdrawn but will not be matched. |

| Duration of suspension or trading halt | A suspension may persist for a prolonged period. | A trading halt is usually intra-day, with a minimum duration of 30 minutes. SGX-ST may extend the duration of a trading halt beyond three Market Days upon the Issuer's request. |

| Upon lifting of suspension or trading halt | Upon lifting of a suspension, the suspended security or futures contract will enter into an Adjust Phase for at least 15 minutes. | Upon lifting of a trading halt, orders that can be matched will be matched at a single price computed based on the algorithm set by SGX-ST. Unmatched orders will be carried forward into the market phase that the market is in when the trading halt is lifted. |

Added on 3 June 20193 June 2019.

Practice Note 8.13.4 and 8.15.7 Approval of Off-Market Trades in a Security or Futures Contract Subject to Suspension or Trading Halt

1.1

This Practice Note explains the rationale and the circumstances under which SGX-ST may approve the trading of a security or futures contract that is the subject of a suspension or trading halt.

Added on 3 June 20193 June 2019.

1.2

Rule 8.13.4 says securities or futures contract that have been suspended from trading shall not be traded on the Trading System. Except with SGX-ST's approval, a Trading Member must not execute any transactions in a suspended security or futures contract.

Added on 3 June 20193 June 2019.

1.3

Rule 8.15.7 says securities or futures contracts that are subject to a trading halt shall not be traded on the Trading System. Except with SGX-ST's approval, a Trading Member must not execute any transactions in a security or futures contract subject to a trading halt.

Added on 3 June 20193 June 2019.

2.1

All market participants should have equal opportunity. The objective of a suspension and trading halt is usually to facilitate proper dissemination of material information to the market place to ensure the operation of a fair market. Hence, SGX-ST Rules 8.13.4 and 8.15.7 stop all trading of a security or futures contract by a Trading Member if the security or futures contract is under suspension or trading halt. However, SGX-ST recognises that there may be circumstances under which off-market trading of the security or futures contract is appropriate.

Added on 3 June 20193 June 2019.

3. Circumstances under which SGX-ST may approve off market trades in a security or futures contract subject to suspension or trading halt

3.1

SGX-ST may, on a case-by-case basis, approve off-market trades in a security or futures contract that is subject to suspension or trading halt, if the buying customer and selling customer are informed of the reasons for suspension or trading halt and there is a reason for the trade beyond simply wanting to trade. Circumstances under which SGX-ST may approve off-market trades include:

Added on 3 June 20193 June 2019.

Practice Note 9.6.4(b) Money Received on Account of Customer

Added on 3 June 20193 June 2019.

1.1

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

1.2

Rule 11.3 sets out the procedures for the cancellation of Error Trades. This Practice Note further sets out the steps that a Trading Member should take if it wishes to cancel an Error Trade.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

1.3

This Practice Note also sets out the procedure when SGX-ST cancels a contract arising from a Trade at Close.

Added on 3 June 20193 June 2019.

2.1.1

Rule 11.2.1 states that an "Error Trade" refers to a trade that is executed on the Trading System and that results from:

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.1.2

For the purpose of this Practice Note, the party that caused the Error Trade will be referred to as the "TM in error"; any counterparty to the Error Trade will be referred to as a "counterparty TM"; and both parties will be referred to collectively as the "parties".

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.2.1

When an Error Trade occurs, the TM in error must:

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.2.2

Both the TM in error and the counterparty TM(s) must take all necessary steps to minimise any likely market impact caused by the Error Trade.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.2.3

Rule 11.4.1 gives SGX-ST the discretion to review any Error Trade if SGX-ST deems it necessary for the proper maintenance of a fair and orderly market. As such, market participants are advised that even if they do not initiate the procedure for cancelling an Error Trade, SGX-ST may exercise its discretion under Rule 11.4.1 to review the Error Trade.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.3.1

Upon being notified by a TM in error of an Error Trade, the counterparty TM must contact all its affected clients to:

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.3.2

In the event that the parties agree to cancel an Error Trade, the following procedures will apply:

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.3.3

If the counterparty TM agrees to cancel an Error Trade, the TM in error should consider compensating, on an ex gratia basis, the counterparty TM for any losses that would be incurred as a result of the mutual cancellation.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.3.4

If the parties cannot mutually agree to cancel the Error Trade, the TM in error may submit a written request to SGX-ST to review the Error Trade.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.3.5

In making the request to SGX-ST to review an Error Trade, the TM in error must:

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.3.6

In a situation where multiple counterparty TMs are involved in an Error Trade and some agree to a mutual cancellation while the others do not, the TM in error must notify all the counterparty TMs of any referral to SGX-ST for review.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.3.7

If a TM in error makes a request to SGX-ST to review an Error Trade, the counterparty TM must provide the TM in error and SGX-ST with its reasons for not agreeing to a mutual cancellation of the Error Trade.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.3.8

The timeframe referred to in paragraph 2.3.5 for the TM in error to make the request to review an Error Trade is to minimise the impact of any cancellation on the market. In this regard, SGX-ST reserves the right not to facilitate any request to review an Error Trade if SGX-ST receives the request after the said timeframe.

Added on 3 June 20193 June 2019.

2.4.1

A TM in error must pay a non-refundable trade review fee of S$1,000 for each referral accepted for review by SGX-ST, regardless of the outcome of the review.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.4.2

In its referral to SGX-ST for review, the TM in error shall provide details of:

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.4.3

Once SGX-ST has reviewed an Error Trade, SGX-ST will inform the market of the outcome of the review (i.e. whether the Error Trade remains valid or has been cancelled) through various media which may include but not be limited to the use of market broadcast and publication on any website by SGX.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.4.4

SGX-ST will also notify the parties of the outcome of the review in writing.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.5.1

Rule 11.4.1 gives SGX-ST the discretion to review any Error Trade if SGX-ST deems it necessary for the proper maintenance of a fair and orderly market, notwithstanding any no-cancellation range.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.5.2

Rule 11.5.3 states that SGX-ST has the discretion to apply or remove a no-cancellation range.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.5.3

Market participants are advised that an Error Trade may be cancelled by SGX-ST even if the Error Trade falls within the no-cancellation range.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

2.6.1

SGX-ST may in its discretion allow for an extension of time for any submission of information and documents in relation to the Error Trade, particularly during the review stage.

Added on 3 June 20193 June 2019 and 3 June 20193 June 2019.

3.1.1

If SGX-ST cancels a contract arising from a Trade at Close, SGX-ST will inform the market of the cancellation through various media which may include but not be limited to the use of market broadcast and publication on any website by SGX.

Added on 3 June 20193 June 2019.

3.1.2

Subsequently, SGX-ST will notify both parties to the Trade at Close in writing of the cancellation.

Added on 3 June 20193 June 2019.

1.1

Rule 11.5.5(c) provides that SGX-ST may, in its discretion, use an alternative price as the Reference Price for the no-cancellation range if (a) the price of the last good trade is not available; or (b) SGX-ST deems the price of the last good trade to be unreliable or inappropriate as a Reference Price.

Added on 3 June 20193 June 2019.

1.2

In normal market conditions, the price of the last good trade is adopted as the Reference Price. However, SGX-ST has considered that there may be situations where the price of the last good trade is not available or not appropriate. In such situations, SGX would seek to establish a Reference Price from alternative sources.

Added on 3 June 20193 June 2019.

1.3.

This Practice Note sets out the alternative prices that SGX-ST may consider in establishing the Reference Price when the price of the last good trade is inappropriate.

Added on 3 June 20193 June 2019.

2.1.

For all securities except bonds and structured warrants, SGX-ST may use any of the following alternative prices as the Reference Price for the no-cancellation range.

Added on 3 June 20193 June 2019 and amended on 30 May 2023.

2.2.

In addition, SGX-ST may also use the alternative prices set out in the table below for the instruments stated:

| Instrument | Alternative prices that may be used as the Reference Price |

| Extended settlement contracts | • The price of the last good trade in the underlying stock. |

| Depository receipts | • The previous closing price of the underlying instrument in home market. • In the case of ADRs, the previous closing price of the ADR in the US market. |

| Exchange traded funds | • The previous closing price as determined in accordance with Rule 8.3. • The average of the last quoted bid price and the last quoted offer price for the exchange traded fund immediately preceding the error trade. The selection will not include the quotes provided by the Designated Market-Maker who is involved in the error trade that is under review. • The indicative net asset value. |

| Exchange traded notes | • The average of the last quoted bid and the last quoted offer price for the exchange traded note immediately preceding the error trade. The selection will not include the quotes provided by the Designated Market-Maker who is involved in the error trade that is under review. • The price of other debt papers with a similar credit rating. |

Added on 30 May 2023.

2.3.

Where any of the prices set out in paragraphs 2.1 and 2.2 is denominated in a currency different from that of the instrument on SGX-ST, SGX-ST may apply such exchange rate factor as it deems appropriate.

Added on 30 May 2023.

3.1.

Where SGX-ST determines that an appropriate Reference Price cannot be established, it will not establish a no-cancellation range.

Added on 3 June 20193 June 2019.